The moral justification of capitalism rests upon one very simple assumption:

If you work hard you will get ahead. Remove this promise and work becomes, as was the case for

Sisyphus, little more than drudgery.

Unfortunately, since the mid-1970s the moral justification of capitalism in America has slowly begun to disappear. In very simple terms, while productivity and

national income has surged wages and benefits have

effectively stagnated for the middle class.

What this means in lost wages and collapsing purchasing power for the average American worker, and America's middle-class, is staggering.

Let's assume that you are making $637 per week in 2013. Now consider this. If wages and benefits had kept pace with the amount of goods and services that you and every other American worker has helped produce over the past 40 years

you would be earning almost $1,200 per week!

Put another way, wages in America have not kept pace with rising productivity and, in some cases, have even fallen. The result of

stagnating wages in America has been

rising debt

loads which has the American consumer on the ropes. As I pointed out

here 10 months ago:

Another way to think about all of this is to think of credit card use in historical terms. If we take what all Americans owed to the credit card industry in 1969 and average it we learn that each household owed $37 in credit card debt. If we do the same thing for 1980 we find that each household owed $670. By 2010 the average household owed $7,800 (but slightly less in 2012).

But wait, it gets worse. While total consumer debt in America has declined by $100 million since 2008, collectively we still owe

$11.4 trillion - with over $1 trillion of this amount considered delinquent. All of this helps explain why bankruptcy

filings in America has averaged about 1.3 million a year since 2003.

At the end of the day, the American worker is treading water financially and effectively

tapped out.

The point here is to let you know that as our nation's economic pie has grown - and

it has grown significantly - America's middle-class is no longer sharing in the fruits of our nation's

growing economy, as was the case between 1945 through the mid-1970s. People are working

just as hard, or harder, than they were

twenty years ago but they are not getting ahead.

With stagnating wages and growing debt loads it's clear that the moral justification of capitalism in America is clearly in trouble. And if it's in trouble America is in trouble. If we are going to properly address this new American reality - assuming that we want to - we need to understand one thing: Why it's important that everyone who works hard has a legitimate shot at getting ahead.

A little bit of history is helpful here.

BEFORE THE MORAL JUSTIFICATION

Feudal and imperial societies from the past are examples of social orders that did not systematically reward hard work or provide opportunities for advancement. Worse, these societies would regularly grant special privileges to aristocrats, the clergy, and to royal family members.

Apart from being burdened by custom, tradition, and foolish superstitions these pre-modern systems were rigged with tax exemptions and legal codes that rewarded the noble airs and established positions of societal elites and their sycophantic courtiers. In a few words, opportunity and reward were only available to those with access to palace networks (elites), social position (the military and the church), or bloodline (aristocracy and monarchies).

Opportunities and market rewards were even more elusive if you were a woman.

In all, up to 90 percent of those living in pre-19th century societies were largely condemned to the low social positions they were born into.

The unwillingness of monarchs and aristocratic tyrants to correct these inequities with systems of education, equal protection under the law, or by providing

sufficient aid to the poor who were condemned to servitude in perpetuity undermined both opportunity and reward. Worse, gaps in wealth and justice were viewed as the natural order of things because, if you listened to the elites of the day, not only did God want it that way but your reward would come in the afterlife.

Before 1776 virtually every society ignored the imbalances and misery that made up the reality of feudal societies around the world. The result was that those who led precarious lives and worked the hardest before the modern era could not reap the fruits of their labor.

Because of a revolution in thinking, and developments in the New World, this situation would begin to change by the 18th century.

ROOTS OF THE CAPITALIST REVOLUTION

Once the Enlightenment began producing learned scholars and critics who questioned the status quo our political and economic world began to change. The idea that people should be free to choose what they wanted to do with their lives both politically and economically put a primacy on creating a system of opportunities for the common man.

Indeed, the primary goal of the American Revolution was to rid the continent of an antiquated imperial system that supported Britain's privileged elite, but restricted the opportunities and rewards available for those in America. Tired of being told what to produce, and on whose terms their goods could be shipped, the primary goal of the America's Founding Fathers was to create a constitution that would guarantee and open up opportunities for the common man in America (as long as you were a white male).

What set the stage for promoting opportunity and reward were ideas about human dignity and personal freedom, which had percolated down from the Renaissance, the Reformation, and the Enlightenment.

These ideas, coupled with the American Revolution would help inspire political upheavals and the liberal constitutions that swept through Europe and Latin America during the 18th and 19th centuries.

Led by the American and French Revolutions, the new social orders - and the new social contracts - that were created released large segments of society from the shackles of feudalism. Dynamic checks and balances replaced stifling customs and traditions. The result was that talent and merit, rather than social position and bloodline, became dominating features of the modern world.

Individual liberty, then, was not just a rallying call for removing the British, and other imperial states. Liberty was necessary to establish both opportunity and the rules behind our new political and economic systems. Being free to choose who would rule over you, and having the liberty to determine what you wanted to make of your life, meant opportunity and reward were built into our new liberal constitutions (again, women, people of color, and indigenous cultures were left behind).

Democracy and free markets were the result.

But just as democracy had its fits and starts (especially with women and Black Americans disenfranchised), a funny thing happened on the way to the market economy that we enjoy today.

FREE MARKETS WITH FEW OPPORTUNITIES, AND NO MORAL COMPASS

Today we know that opportunity and market rewards in the past were undermined by

feudal customs,

traditions, and

entrenched privileges.

Fraud and

political schemes would also worked to undermine opportunity and market reward, as it does today (more on this below).

While the penchant to defraud and scheme appears to be a human constant, the moral justification of capitalism in post-colonial America was also undermined by our societies

new customs and

beliefs. Specifically, slavery and social mores would turn blacks, women, and even children into second class citizens as a matter of course.

Ascribed gender roles, slavery, and simple ignorance not only torpedoed the earning capacity of these groups, but they robbed women, children, and generation after generation of blacks in America of an opportunity to earn and accumulate wealth.

While many used tradition, the Bible, and

even junk science to justify ascribed gender roles, exploitation, slave markets and, later, even Jim Crow, one thing was very clear: Free markets in America developed and prospered with no moral compass, and with few opportunities for a large segment of the population.

The reality is that wages and wealth accumulation in the United States were skewed to favor white males. Their accomplishments and market rewards in the 18th and 19th centuries, which are often attributed hard work and business acumen alone, is a misleading story line.

Their successes were made possible by a set of rules that made it clear that white males were privileged and protected by custom and law.

White males did not have to worry about competing against more than half the population because opportunities for women to compete on a level playing field were denied. Nor did white males have to worry about competing against black Americans. Slavery and, later, Jim Crow took care of this. The legal and social exclusion of more than one-half of America's workforce from the marketplace was the ugly reality of America's "free market" system.

Adding to these free market realities was the prevalence of child labor. Unable to escape the feudal notion that children should contribute to the family’s well-being (an accepted practice as long as we're talking about herding sheep, or caring for a sibling on a farm), children were put to work in factories and mines at the beginning of the industrial revolution.

The moral questions of child labor were famously raised by Charles Dickens in

Oliver Twist, and, later, chronicled by E.P. Thompson’s

The Making of the English Working Class (1963). Still, during the initial stages of industrialization many argued that children were “free agents” capable of negotiating salaries and work conditions on their own behalf.

But what chance did a 12 year old child working in the mines have? Uneducated and often frail, children had few skills, and even fewer options.

For most hard working women, children, and people of color in 19th century America opportunity and reward were elusive, at best. Put more simply, the moral justification of capitalism in America

did not exist.

Progressive political movements would slowly push "the state" to change this reality.

FULL OPPORTUNITY AND REWARD ARRIVES IN AMERICA (kind of)

For many it’s tempting to say, “That’s just the way things were. Those who did compete still found an unrelenting system that fostered the ‘survival of the fittest’ mentality. These people were ‘survivors’ in the Darwinian sense …”. While this may be true it also ignores the logical follow-up: Those who participated and prospered in eighteenth and nineteenth century America did so in a system that systematically bottled up the prospects of more than one-half of society.

Put another way, the game was rigged, and the benefits flowed one way.

As such, we can’t attribute great success, wealth levels, and pay disparities in America after the American Revolution to efficient capitalist market forces. The analysis is incomplete. We have to acknowledge that well over one-half of America's population could not compete on a level playing field during the first 175 years of America's existence.

What this means is that the moral justification of capitalism is not simply a function of freedom, or saying we have open markets and free trade. The state has had to step in and make sure that those who work hard are not excluded from the rewards and opportunities available to others. Being rewarded with fairly negotiated wages and benefits doesn't just happen because you have a competitive market environment where goods are bought and sold.

The American experience makes this clear on so many levels.

Slaves and people of color needed a civil war and a civil rights movement to gain access to market rewards. Women and children needed social justice and legal protections to find their opportunities in the workplace and through education. There were no “invisible hands” involved in making market opportunities available to all. The state had to force the issue.

Today, the scourge of child labor, Jim Crow and gender bias have been dealt with on many levels in America. It's not fixed, but it has been dealt with. Still, other factors continue to eat away at the moral justification of capitalism today.

WHY "THE MORAL JUSTIFICATION ..." STILL NEEDS WORK

One way to stack the deck for, and against, certain groups is to use political institutions to secure favors. This is happening today in America. Favorable legislation, government subsidies, market protections, stacked regulatory agencies, government supported attacks on labor, tax burdens shifted to the middle class, and regular industry bailouts are all examples of this.

But this shouldn't come as a surprise. The intellectual godfather of capitalism, Adam Smith, understood that the state would pick favorites. This is why he made it clear that there should be minimal government intervention in the marketplace. It's not to allow market players to do what they want, as many misinformed pundits and politicians like to claim, it's because - as Smith pointed out - government usually intervened on behalf of those with power and privilege.

When this occurs, the reward and incentive system is just as skewed as it was when child labor, Jim Crow, and ascribed gender roles were the order the day. While favorable legislation may not be as socially demeaning as gender bias or Jim Crow, the economic effect is similar: Market rewards are unduly skewed, while opportunities are compromised.

As long as bailouts, artificially cheap money, and favorable legislation that comes in the form of market protections are the order of the day in America - and it is - it's impossible to speak glowingly of free markets and capitalism in America today.

I'll go one step further. The way the system has been rigged to favor Wall Street over Main Street, the United States does not have a functioning free market system.

WHY THE RIGHT IGNORES WHAT MAKES THE "MORAL JUSTIFICATION" TICK

Market achievements and individual success in America - past and present - owe a great deal to state sanctioned discrimination and social injustices. Simply put, when the government ignores, encourages, or winks at a way of life that helps determine who emerges at the top of our economic food chain the moral justification of capitalism is diluted, if not entirely broken.

This is the case in America today.

We need to acknowledge that financial success in our modern markets has always been influenced by favorable legislation, demeaning stereotypes, and social beliefs that cheapen us all. The notion that “hard nosed” business decisions are what made America and what drives market success is a myth.

Many politicians and pundits today like to downplay (or ignore) the role the state plays in making markets work. They prefer, instead, to put their faith in an incomplete understanding of “markets” and free trade that is based more on myth than historical fact. They do this because it helps inflate their own sense of who they are, especially if they have lots of money.

The reality is

the state creates the conditions under which wealth is created. It always has.

Unfortunately, most market observers don't understand any of this. Like Galileo’s colleagues, who were afraid to look in his telescope for fear of what they might see, many

laissez-faire market proponents do not want to look at (or acknowledge) the role of the state in making markets work.

In terms that Galileo would understand, having to acknowledge the role of the state in setting the table for wealth creation would turn their very linear and flat world round, which would make it much more complex.

But their reluctance to look through the "state" telescope is understandable. Many people are comfortable only in the world they know. This explains why the beneficiaries of inheritances, family networks, transferred property, and market windfalls made possible by favorable legislation and bailouts would rather believe that their wealth is a product of their acumen and hard work alone.

It reaffirms their belief that individual fortunes are evidence of individual strength and market accomplishments.

This is a myth.

Those who are making a fortune on Wall Street - while benefiting from U.S. tax payer backed bailouts, artificially cheap money, and favorable legislation - don't want anyone looking behind the capitalist curtain that surrounds their achievements. What they fear is what the rest of us already know. Our current legal system and modern moral code not only makes their kind of wealth possible but - as French economist Frederic Bastiat (1801-1851) might have suggested - it glorifies the end result, no matter what the means.

What this ignores is what Adam Smith had to say about liberty and what he called the laws of justice. He made it clear (as I point out in my book, p. 16) that deliberately shifting "a greater share" of resources to an industry than would naturally go to it would retard "the progress of society toward real wealth and greatness."

This is what's happening in America today.

CONCLUSION ...

After World War II the state was instrumental in making sure that almost everyone who worked hard could find the opportunities to get ahead. Then, suddenly, the state came under political attack more than 40 years ago and began to reverse this course. Specifically, it began to promote the interests of Wall Street and industry over the interests of Main Street and working class America.

Not surprisingly, markets are no longer working for middle-class America because the state has been taking sides, to an extreme. This is one of the reasons why the moral justification of capitalism in America has been collapsing over the past 40 years. It's one of the reasons why wages for Main Street have not kept pace with our nation's growing levels of productivity.

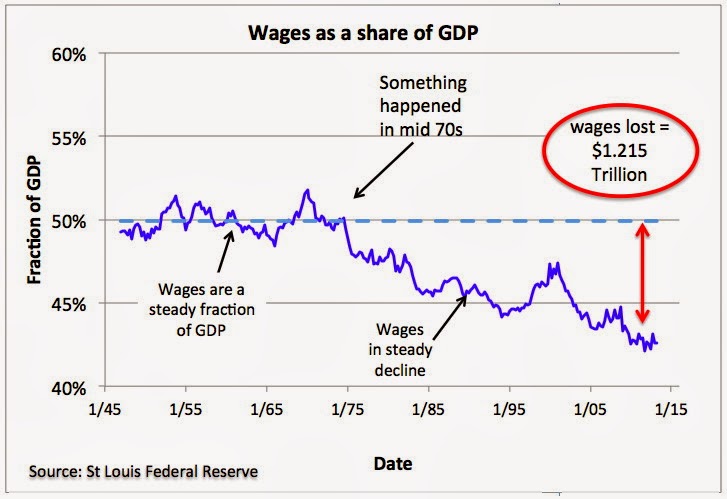

Think about it. As I noted at the beginning of this piece, if middle-class wage earners salaries had kept pace with productivity hikes the way they did immediately after WWII someone making $637 per week today would be making an additional $500 a week more. America's national income has grown by

more than $12 trillion as productivity and profits have surged, yet wages as a share of national income

has actually dropped.

The impact has been significant.

According to data from the Federal Reserve of St. Louis America's middle-class has lost about

$1.215 trillion in wages over the last 40 years (which, not so coincidentally, is slightly above what Americans

borrowed and owed to the credit card industry when the market collapsed in 2008).

At the end of the day, Adam Smith believed individuals should be free to trade, but only as long as everyone would abide by the same laws of justice. This means no favorable legislation, no regular bailouts, and definitely no artificially cheap money for one group.

The moral justification of capitalism is under attack in America. And it's not coming from the "socialists" or the communists. It's coming from a small group of people who believe the state has nothing to do with their wealth, and the political sycophants in the media and in the halls of Congress who think they are right.

The gap that exists between the theoretical promises of capitalism and the practical realities of our markets is wide, and getting wider. And it's because the moral justification of capitalism in America is on the ropes.

- Mark

{kind=link}