Arrgh ... If I hear one more GOP presidential hopeful blame our current market mess on President Obama again I think I'm going to have a brain aneurysm. To be sure, I understand the political part of what the candidates are doing. What gets me is how so many Americans buy into the ignorance and stupidity, and it's starting to burn through the electorate like wildfire ...

I bring this up because people speak as if President Obama could have somehow waved a magic wand and fixed the economy in just three years. Apart from having to deal with a "just say no" GOP, what they forget is that it took the better part of 6 years for the Bush administration and a GOP-led Congress to blow through budget surpluses and set the stage for burning down our economic house.

Destroying the peace and prosperity that was left to President Bush took some real effort and incompetence, and can't easily be undone.

So, in an effort to dispel any notion that President Obama is to blame for our current mess (though, I agree, he screwed up on bailing out the banks), I'm going to present what I hope is an easy ten point overview of why the market collapsed in 2008. What you'll see is that our current economic mess didn't happen over night, and won't be turned back over night either. I'm drawing the information straight out of my book. So if you want more information go out and buy my book (I know, shameless plug).

As you'll see, there's enough bi-partisan stupidity to go around, though one party definitely deserves more blame than the other for our current mess. You can quibble with the 10 points (I might even emphasize one point over another in the future), but the general outline of our market collapse, and what ails our markets today, are here.

Anyways, here goes. Our market collapse, in ten easy steps ...

______________________________________

THE BEGINNING

1.

A Naive Belief in "Free Market" Ideology (blinds policymakers)

... Ronald Reagan enters the White House after Maggie Thatcher becomes Britain's Prime Minister. Trickle Down economics is born. Deregulation, tax cuts for the rich, and globalization are embraced.

... After dumping trillions in borrowed money into the economy Reagan almost triples the national debt, raises taxes on the middle class (FICA), and lifts the debt-limit ceiling 17 times. Yet he's hailed as a fiscal conservative.

... In an effort to concentrate on "free markets" in the 1980s, U.S. leaders effectively ignore economic costs associated with (1) paying for the defense of the west, (2) America's rude introduction to unbridled globalization (caused, in part, by the success of Bretton Woods), (3) the structural changes in the economy caused by the rise of financial services sector (i.e. the "symbolic" economy), (4) Nixon's price controls, and (4) OPEC's inflation inducing price hikes.

... Instead of dealing with costs of U.S. militarism, competition from abroad, the financialization of the economy, Nixon's price controls and OPEC price hikes, America's leadership blames sluggish U.S. economy on "the state" (regulations, domestic programs, and taxes), while calling for "a good 'ol shot of capitalism" in 1980.

BUILD UP: 1970s-1980s

2.

Deregulation / Financialization of Economy (regulator vacation)

... 1971 the dollar is de-linked from gold and becomes a commodity. Futures markets develop for money, interest rates, and other novel investment tools of the trade.

... OPEC price hikes wreak havoc on markets and prices. Pundits and foreign policy experts alike (see especially Henry Kissinger) are caught flat footed.

... new policies and

deregulation pushed by financial services sector make the Savings & Loan debacle possible (1970s/1980s), and help to set the stage for the

deregulation stupidity that eventually leads to the dismantling of the Glass-Steagall Act and the passage of the Financial Services Modernization Act (1999)

... financial services sectors consolidates as symbolic economy grows in importance. SEC begins its disappearing act.

3.

Interest Rate Manipulation (what free market?)

...

Interest rates are used first to stabilize markets, and then as a tool to stimulate them. Bailouts and money dumps begin in earnest under Alan Greenspan's leadership at the Federal Reserve. The Greenspan Put (dumping cheap money into the system when Wall Street gets in trouble) begins in 1987.

... Federal Reserve becomes

Wall Street's support system, and then it's puppet.

... Market recklessness surges as financial services (and gambling) grows.

4.

Yield Hunts / Secondary Markets (casino economy begins)

... Inflation + low interest rates in 1980s lead bond traders to start looking for higher yield investments.

... Non-traditional investment products become more attractive, but market players are (initially)reluctant because of low bond ratings.

... Globalization (largely unregulated) allows financial firms to seek higher investments abroad through loans, secondary markets, arbitrage, etc.

5.

Bailout City (what, accountability?)

... Beginning with

Mexico in 1982 (actually it begins earlier, but this is where I'm starting), Wall Street's stupidity is bailed out time and time again. The Greenspan Put begins in earnest in 1987 with LTCM.

... Accountability and free market ideology are undermined with bailouts, but no one cares. Wall Street/investment bankers continue to believe in the wonders of the market.

MANIA: 1990s / Aughts ...

6.

Securitization / Derivative Markets Explode (hello Rumpelstiltskin)

... Market players become Rumpelstiltskin, and turn crap into gold. CDOs, SIVs, CDSs, and other novel investment products become popular, especially after ratings agencies get into bed with Wall Street's biggest investment banks.

Interconnected market players game the system.

... Wealth extraction becomes more important than wealth creation. What would have been criminal or fraudulent before becomes

modus operandi with favorable legislation.

... Security markets begin demanding more products (i.e. debt) to securitize, as rating companies begin to hand out AAA ratings on virtually anything that can be chopped up and modeled.

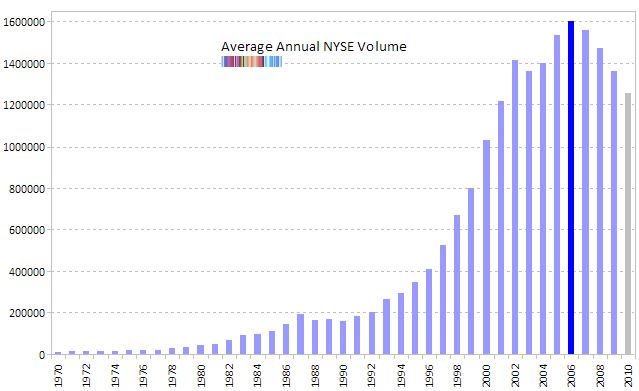

... Symbolic economy grows 30-40 times the real economy.

7.

Toxic Market "Innovations" Applauded (herd mentality for rugged individualists)

... Wall Street (Goldman Sachs then-CEO, Hank Paulson) goes to SEC for permission in 2004 to carry 40:1 debt to equity ratios (Imagine going to a bank and asking to borrow $2 million on a $50,000 a year income). It's granted.

... With demand for securities growing, hedge funds,

shadow banks, and

Wall Street press Washington regulators to allow "non-conventional" lender packages into the housing market.

... Non-bank, or

shadow banks, become critical cogs in financial machine. Subprime mortgage underwriters ignore all lending standards.

... With brokers dumping newly created loans 30-60 days after they're written, NINJA loans, No Doc loans, Liar loans, and other type of teaser programs become the norm.

... Caution thrown to the wind as competent regulators like

Brooksley Born are buried politically (after she called attention to disastrous derivative markets), and Sarbanes-Oxley legislation allows Washington/Wall Street to say "See, we fixed it" after Enron. Free market praised as fraud & lack of oversight become the norm.

... Consumers borrow and use homes as ATMs, which give the illusion of prosperity.

... Personal debt climbs; Bush doubles the national debt. Bubbles and record profits grow.

8.

The Federal Reserve / Congress Become Cheerleaders (casino economy goes Vegas)

... Cheerleaders (who should be regulators) applaud innovative instruments and massive (unregulated) lending as evidence of the power of unrestrained markets.

... Home equity loans explode, consumption increases. Debt is the name of the game as it provides source for new securities and credit default swaps (insurance).

... Alan Greenspan cheers "new paradigm of active credit management" as

interconnected institutions and the shadow banking system sign off on new securities, mortgage back contracts, and other debt instruments/loans.

... Wall Street and financial services sector pay and bonuses shoot through the roof.

... Notional value of contracts surge past $285 trillion (when annual GDP is only $14 trillion).

PAYING THE PIPER: The Mother of All Bailouts

9.

Boom / Bust / Credit Freeze (back to reality)

... What do you know? Strawberry pickers making minimum wage really can't afford $700,000 home loans.

10.

Blame Game Begins (continues today)

... Government Secured Enterprises (Fannie Mae), FHA loans, and Community Reinvestment Act (the poor) originally blamed for market collapse. Former Treasury Secretary

Hank Paulson joins the game.

... George W. Bush (

wrongly) claims he inherited a recession, and left with a recession. Nothing to see here. What a loser.

... Much anticipated bi-partisan FCIC report is

blind-sided by

GOP primer that deliberately excludes any mention of

Wall Street, the

shadow banks,

interconnected cronyism, and

deregulation (all the stuff I highlighted in red above).

______________________________________

The incredible thing is that we have now come full circle. Today, Republican presidential candidates are full fledged free market ideologues, pushing for more of the same policies that got us into our current mess. Don't believe me? Start at #1 above. Begin reading, again.

Only this time the banks and Wall Street are the only ones who have access to, and are profiting from, unlimited cheap money and

our propped up casino economy. Think about it. Today the house of cards (yes, it's still a house of cards) is propped up by cheap money for Wall Street, deregulation for Wall Street, favorable legislation for Wall Street, and

adherence to a failed ideology in Washington that keeps the trillion dollar bailout and

QE money flowing, for Wall Street.

At the end of the day it took almost a full generation to reach our current level of market stupidity. It's not going to end under President Obama in one term. Especially with the GOP acting like a political

boat anchor.

- Mark