In spite of ruining the economy with toxic instruments that few understood, and even fewer saw traded, the financial institutions who helped wreck our economy are lobbying Congress hard to keep things as they were.

In this NY Times' article, "Even in Crisis Banks Dig in for Battle Against Regulation," Gretchen Morgenson explains how the financial institutions are fighting so that they can keep on trading Credit Default Swaps (CDS) with few oversights. In a few words CDS are insurance contracts that must be paid out once the insured product fails to perform. For example, if you have a group of "insured" mortgage contracts bunched together (a security) that go under because people are no longer making payments on their homes (a default) whoever provided insurance on the mortgage contracts are supposed to pay out.

The companies who wrote CDS contracts before the meltdown - AIG, Merrill Lynch, and Citigroup, among others - wrote so many contracts that when the market collapsed they couldn't pay out the insurance policy (today, the CDS market insures transactions with a face value of $600 trillion). In essence, the banks only wanted the monthly payments that came from the "insured" parties but never intended on paying on the insurance policy when things got bad.

The banks and other financial institutions were able to write so many insurance contracts because they were unregulated. Put another way, no one was watching them as they wrote contracts that they couldn't cover, and would not honor. This is the world the banks want to see continued.

Treasury Secretary Tim Geithner wants to help the banking industry along by allowing them to continue operating in secret by calling for greater oversight while, incredibly enough, he also pushes for the Mother of All Loopholes - allowing a category of "customized" CDS contracts to continue operating in the dark.

When asked by Sen. Tom Harkin (D-Iowa) to define a "customized" swap Tim Geithner's response was stunningly pathetic. He told Sen. Harkin he would have to get back to him.

- Mark

As an aside ... The real travesty here was that the prospect of CDS "insurance" down the road encouraged the knuckleheads who were writing NINJA (No Income, No Job, No Assets) and other unrealistic mortgages to continue issuing these kind of loan contracts. And why not? The contracts would be "insured," right?

Sunday, May 31, 2009

DICK CHENEY ... A LIAR AND A COWARD

In yesterday's program I made it clear, once again, that former VP Dick Cheney is a liar and a coward. Cheny's five deferments during the Vietnam War and his constant whining about being scared are proof of his cowardice. I should have carried the discussion through to chronicle Dick Cheney's lies and distortions, but we were running out of time. I'm fixing that now.

In this McClatchy News article ("Cheney's speech ignored some inconvenient truths") Jonathan S. Landay and Warren P. Strobel outline ten lies that Dick Cheney made during his "national security" presentation. Here's their take on one of them:

Landay and Strobel point out that Cheney ignored that a "top-secret 2004 CIA inspector general's investigation found no conclusive proof that information gained from aggressive interrogations helped thwart any 'specific imminent attacks' ... ". Cheney also ignored that in December FBI Director Robert Mueller told Vanity Fair magazine that he didn't think that the techniques disrupted any attacks.

There's more lies and distortions so I encourage you to read the Landay and Strobel piece. Why anyone would want to listen to this coward is beyond me. I also encourage you to read Frank Rich's, "Who Is to Blame for the Next Attack." Rich makes it abundantly clear that it won't be President Obama.

- Mark

In this McClatchy News article ("Cheney's speech ignored some inconvenient truths") Jonathan S. Landay and Warren P. Strobel outline ten lies that Dick Cheney made during his "national security" presentation. Here's their take on one of them:

[Cheney] quoted the Director of National Intelligence, Adm. Dennis Blair, as saying that the information gave U.S. officials a "deeper understanding of the al Qaida organization that was attacking this country."More specifically, Cheney was trying to conflate torture with saving lives from imminent attack by saying that the current Director of National Intelligence (who oversees the CIA, the FBI, and the other 14 intelligence gathering agencies we have) agrees with him on the effectiveness of torture.

In a statement April 21, however, Blair said the information "was valuable in some instances" but that "there is no way of knowing whether the same information could have been obtained through other means. The bottom line is that these techniques hurt our image around the world, the damage they have done to our interests far outweighed whatever benefit they gave us and they are not essential to our national security."

Landay and Strobel point out that Cheney ignored that a "top-secret 2004 CIA inspector general's investigation found no conclusive proof that information gained from aggressive interrogations helped thwart any 'specific imminent attacks' ... ". Cheney also ignored that in December FBI Director Robert Mueller told Vanity Fair magazine that he didn't think that the techniques disrupted any attacks.

There's more lies and distortions so I encourage you to read the Landay and Strobel piece. Why anyone would want to listen to this coward is beyond me. I also encourage you to read Frank Rich's, "Who Is to Blame for the Next Attack." Rich makes it abundantly clear that it won't be President Obama.

- Mark

Saturday, May 30, 2009

THE COSTS OF "BIGNESS"

The Financial Times is reporting that the "four biggest US commercial banks – JPMorgan Chase, Citigroup, Bank of America and Wells Fargo – possess 64 per cent of the assets of US commercial banks."

Why is this significant? Because it's un-democratic and corrodes free market principles by robbing local market players of the ability to make the call about a consumers ability to pay.

Why is this significant? Because it's un-democratic and corrodes free market principles by robbing local market players of the ability to make the call about a consumers ability to pay.

Think about the local banker who might know and care that you had your identity stolen and that your accounts were cleaned out. But you still have a job. If you go by the books of one of the big banks you're out of luck and probably will not get financing for a new home. Conversely, I have to think that a local banker would have caught on to the fact that a local applicant didn't have a real job, or income, and most likely would not have granted the mortgage loans that we consider toxic today. Even the knowledge that Fannie Mae was going to buy up the loan may not have swayed the local banker because the local banker has to live with the consequences of a series of failed loans in his or her community.

In nakedcapitalism.com's "Review of Karl Polanyi's The Great Transformation" Joe Costelo points out that concentrating economic power in the hands of a few banks has reduced or robbed the market system of the capacity to make judgment calls about the viability of small businesses and regular homeowners. Community knowledge is important here.

Centralized economic decision-making, which comes when four banks control 64% of all the assets managed by commercial banks, has led to an over reliance on mathematical models to approve people who don't deserve more credit and new fangled super instruments that no one really understands.

As I was reminded by one of my students, it has also led to the rise of "unsecured debt" like credit cards, which the models say are OK, which condem people (esepecially the young) to economic serfdom.

Worse, "bigness" and centralized economic power have allowed a few financial players to dominate our political process and secure favorable legislation. This undermines both democracy and the integrity of markets.

- Mark

Why is this significant? Because it's un-democratic and corrodes free market principles by robbing local market players of the ability to make the call about a consumers ability to pay.

Why is this significant? Because it's un-democratic and corrodes free market principles by robbing local market players of the ability to make the call about a consumers ability to pay. Think about the local banker who might know and care that you had your identity stolen and that your accounts were cleaned out. But you still have a job. If you go by the books of one of the big banks you're out of luck and probably will not get financing for a new home. Conversely, I have to think that a local banker would have caught on to the fact that a local applicant didn't have a real job, or income, and most likely would not have granted the mortgage loans that we consider toxic today. Even the knowledge that Fannie Mae was going to buy up the loan may not have swayed the local banker because the local banker has to live with the consequences of a series of failed loans in his or her community.

In nakedcapitalism.com's "Review of Karl Polanyi's The Great Transformation" Joe Costelo points out that concentrating economic power in the hands of a few banks has reduced or robbed the market system of the capacity to make judgment calls about the viability of small businesses and regular homeowners. Community knowledge is important here.

Centralized economic decision-making, which comes when four banks control 64% of all the assets managed by commercial banks, has led to an over reliance on mathematical models to approve people who don't deserve more credit and new fangled super instruments that no one really understands.

As I was reminded by one of my students, it has also led to the rise of "unsecured debt" like credit cards, which the models say are OK, which condem people (esepecially the young) to economic serfdom.

Worse, "bigness" and centralized economic power have allowed a few financial players to dominate our political process and secure favorable legislation. This undermines both democracy and the integrity of markets.

- Mark

Friday, May 29, 2009

POLITICAL RABIES HITS THE GOP?

As we move through the Supreme Court confirmation process of Sonia Sotomayor I would have to say that the best overview of how unhinged the Conservative smear camp has become are the pieces put together by MSNBC's Rachel Maddow. Here's a 12 minute clip from tonight's program that puts much of it in perspective. In a few words, like an animal with rabies, the party of Rush-Newt-Cheney attack with little or no thought for what they are doing.

As Maddow points out, if Conservatives want to disqualify Sonia Sotomayor for her "empathetic" qualities, her "judges make law" comments (making her a "judicial activist"), or because her decisions might be influenced by her ethnicity or upbringing, Conservatives need to also disqualify Supreme Court Justices Alito, Scalia, and Thomas.

For me, however, the real proof that Conservatives have become unhinged and may be afflicted by what can only be called political rabies are comments that refer to Sonia Sotomayor as an "hispanic chick lady" (Glenn Beck) who is both "stupid" (Karl Rove) and "a racist" (Newt Gingrich). For his part, G. Gordon Liddy's threw in the comment that he hopes she's not "menstruating" when she's making big decisions. Rabies, indeed.

I'll be discussing all of this, and more, on Saturday's program.

- Mark

As Maddow points out, if Conservatives want to disqualify Sonia Sotomayor for her "empathetic" qualities, her "judges make law" comments (making her a "judicial activist"), or because her decisions might be influenced by her ethnicity or upbringing, Conservatives need to also disqualify Supreme Court Justices Alito, Scalia, and Thomas.

For me, however, the real proof that Conservatives have become unhinged and may be afflicted by what can only be called political rabies are comments that refer to Sonia Sotomayor as an "hispanic chick lady" (Glenn Beck) who is both "stupid" (Karl Rove) and "a racist" (Newt Gingrich). For his part, G. Gordon Liddy's threw in the comment that he hopes she's not "menstruating" when she's making big decisions. Rabies, indeed.

I'll be discussing all of this, and more, on Saturday's program.

- Mark

OH, WHAT A MESS WE WEAVE ...

Money Morning is one of a handful (or two handfuls?) of investment newsletters that I get on a regular basis. While the ultimate goal of these e-mail newsletters is to sell you their investment products there are several that provide very good market news and political analysis. Money Morning is one of those newsletters.

In this Money Morning review - "Obama Stimulus May End Up Hurting the Economy it Was Supposed to Have Helped" - Martin Hutchinson writes that because President Obama's economic stimulus package adds to our national debt that interest rates are starting to climb. This is not news; it's Economics 101 stuff.

The news lies in the impact that rising interest rates will have on a housing market that is being beaten down by foreclosures and the effect of rising unemployment.

Hutchinson predict that if housing prices continue to fall (which they will; see my "These Guys Still Don't Get It" post below) then "on average every 80% [of] mortgage[s] undertaken since May 2002 ... would be underwater." Let me put this another way - and as a way of emphasizing - the net effect of a continued collapse of housing prices would be that every home owner who purchased a house with 20% down since May 2002 would owe more than it's worth. Why is this scary? Because people will walk away from their homes in droves.

How do you fix this? There are several ways. One, which I've been suggesting over the past year, is to nationalize the failing financial institutions. This would allow the federal government to renegotiate home loans that are under water rather than leaving the job in the hands of a failed industry that is not negotiating in good faith.

Think about it. The U.S. taxpayer is going to get stuck with the bill either way. But I'd rather get stuck with a scenario that stabilizes home ownership (good for Main Street) rather than with a scenario that includes record foreclosures, a wrecked housing market, and subsidies for financial institutions and market players who got us into this mess (which Wall Street wants).

Unfortunately, President Obama listened to Wall Street and ignored Main Street when he left the failing banks in the hands of the morons who got us into this mess. Today they will not negotiate in good faith with homeowners who have stable jobs and who want to stay in their homes because they - and the market players who own a piece of the mortgages - don't want to see the value of their "investment" go down. I'm not sure what this is called, but in my book, this is not capitalism (seriously, read my book, it's not capitalism).

At the end of the day, if the housing market continues to collapse, we need to let Wall Street know that they will also have to pay a price for their greed and stupidity. We can't just let homeowners and the American taxpayer pay for this mess in the form of bankruptcy, foreclosures, wrecked credit and future tax burdens.

- Mark

In this Money Morning review - "Obama Stimulus May End Up Hurting the Economy it Was Supposed to Have Helped" - Martin Hutchinson writes that because President Obama's economic stimulus package adds to our national debt that interest rates are starting to climb. This is not news; it's Economics 101 stuff.

The news lies in the impact that rising interest rates will have on a housing market that is being beaten down by foreclosures and the effect of rising unemployment.

Hutchinson predict that if housing prices continue to fall (which they will; see my "These Guys Still Don't Get It" post below) then "on average every 80% [of] mortgage[s] undertaken since May 2002 ... would be underwater." Let me put this another way - and as a way of emphasizing - the net effect of a continued collapse of housing prices would be that every home owner who purchased a house with 20% down since May 2002 would owe more than it's worth. Why is this scary? Because people will walk away from their homes in droves.

How do you fix this? There are several ways. One, which I've been suggesting over the past year, is to nationalize the failing financial institutions. This would allow the federal government to renegotiate home loans that are under water rather than leaving the job in the hands of a failed industry that is not negotiating in good faith.

Think about it. The U.S. taxpayer is going to get stuck with the bill either way. But I'd rather get stuck with a scenario that stabilizes home ownership (good for Main Street) rather than with a scenario that includes record foreclosures, a wrecked housing market, and subsidies for financial institutions and market players who got us into this mess (which Wall Street wants).

Unfortunately, President Obama listened to Wall Street and ignored Main Street when he left the failing banks in the hands of the morons who got us into this mess. Today they will not negotiate in good faith with homeowners who have stable jobs and who want to stay in their homes because they - and the market players who own a piece of the mortgages - don't want to see the value of their "investment" go down. I'm not sure what this is called, but in my book, this is not capitalism (seriously, read my book, it's not capitalism).

At the end of the day, if the housing market continues to collapse, we need to let Wall Street know that they will also have to pay a price for their greed and stupidity. We can't just let homeowners and the American taxpayer pay for this mess in the form of bankruptcy, foreclosures, wrecked credit and future tax burdens.

- Mark

Thursday, May 28, 2009

ALITO SAID WHAT?

Alioto vs. Sotomayor: A case of double standards?

Here's SC Justice Alito during his confirmation hearings ...

And that’s why I went into that in my opening statement. Because when a case comes before me involving, let’s say, someone who is an immigrant — and we get an awful lot of immigration cases and naturalization cases — I can’t help but think of my own ancestors, because it wasn’t that long ago when they were in that position…

When I get a case about discrimination, I have to think about people in my own family who suffered discrimination because of their ethnic background or because of religion or because of gender. And I do take that into account.

The far right will, no doubt, ignore this Alito clip. Rush, Newt, and the dittoheads are already on a roll. But watch Alito's full comments anyways. You can also see them here.

- Mark

Here's SC Justice Alito during his confirmation hearings ...

And that’s why I went into that in my opening statement. Because when a case comes before me involving, let’s say, someone who is an immigrant — and we get an awful lot of immigration cases and naturalization cases — I can’t help but think of my own ancestors, because it wasn’t that long ago when they were in that position…

When I get a case about discrimination, I have to think about people in my own family who suffered discrimination because of their ethnic background or because of religion or because of gender. And I do take that into account.

The far right will, no doubt, ignore this Alito clip. Rush, Newt, and the dittoheads are already on a roll. But watch Alito's full comments anyways. You can also see them here.

- Mark

Wednesday, May 27, 2009

THESE GUYS STILL DON'T GET IT ...

In this FOX News article, we learn about William Frey, an incredibly shallow and tone deaf market player who wants the courts to guarantee his money by forcing banks to turn away home owners looking to renegotiate home loan terms.

What Frey doesn't seem to understand is that housing markets are crumbling and many of the banks that hold or service mortgage contracts that he's trying to maintain are only solvent because of massive government intervention.

Let me make this clear before I outline how incredibly ignorant and tone deaf this egg-head is: the only reason Mr. Frey has contracts of value to complain about is because the federal government is using taxpayer money so that the entire market does not collapse due to the greed and stupidity of people like him.

Here's the article again.

In it William Frey, who is the president of a company that puts together mortgage-backed securities, recently told the New York Times that he had been contacting banks and threatening to sue them if they renegotiate mortgages for homeowners facing foreclosure. According to Frey, providing better terms for homeowners would mean reducing the value of the mortgage-backed securities held by people like himself. Once the value of the contracts are reduced he stands to lose money.

Here's a couple things Mr. Frey needs to think about:

Later in the article Mr. Frey claims that private hedge funds were to blame for creating the riskiest subprime mortgages. This may be true (but not entirely). Still, Mr. Frey sure wasn't complaining when hedge funds were investing in the real estate market in the process driving up the price of the product that he was putting together and profitting from for years.

As well, Mr. Frey complained about the "strong arm" tactics used by the government to help facilitate the bailout of floundering financial firms (like Citigroup, AIG and Merrill Lynch). He's miffed because some institutions were "strong-armed" into merging with other institutions and taking government money. What Mr. Freey ignores is that the problem the financial sector created with their stupidity and greed is so big that the industry can't unwind many of the complex instruments that people like him helped create.

The toxic garbage has spread throughout the industry like an STD and require forced measures.

There's more. But Mr. Frey needs to keep a couple of things in mind. People are not only losing their jobs but they can do little to nothing as the value (and equity) of their homes collapse. Mr. Frey also needs to keep in mind that at least 1 million Americans will go bankrupt this year while many more see their credit wrecked for years to come. If Mr. Frey wants his "investment" guaranteed he should also be pushing to have the credit and value of each home owner's house guaranteed too. But he doesn't want this. All Mr. Frey is focused on is making sure that his money is guaranteed.

What a standup guy.

At the end of the day Mr. Freey needs to grow up, and learn one thing: there are no guarantees in life. He's not the only one affected by the mess people like him created.

- Mark

What Frey doesn't seem to understand is that housing markets are crumbling and many of the banks that hold or service mortgage contracts that he's trying to maintain are only solvent because of massive government intervention.

Let me make this clear before I outline how incredibly ignorant and tone deaf this egg-head is: the only reason Mr. Frey has contracts of value to complain about is because the federal government is using taxpayer money so that the entire market does not collapse due to the greed and stupidity of people like him.

Here's the article again.

In it William Frey, who is the president of a company that puts together mortgage-backed securities, recently told the New York Times that he had been contacting banks and threatening to sue them if they renegotiate mortgages for homeowners facing foreclosure. According to Frey, providing better terms for homeowners would mean reducing the value of the mortgage-backed securities held by people like himself. Once the value of the contracts are reduced he stands to lose money.

Here's a couple things Mr. Frey needs to think about:

* If you put your money into markets that are inflated that's your problem.In a few words, Mr. Frey needs to realize that he was participating in an inflated and bubble market, like everyone else. Take your lumps.

* If you put your money into markets that were handing out NINJA (No Income, No Job, No Assets) loans like they were candy that's your problem.

Later in the article Mr. Frey claims that private hedge funds were to blame for creating the riskiest subprime mortgages. This may be true (but not entirely). Still, Mr. Frey sure wasn't complaining when hedge funds were investing in the real estate market in the process driving up the price of the product that he was putting together and profitting from for years.

As well, Mr. Frey complained about the "strong arm" tactics used by the government to help facilitate the bailout of floundering financial firms (like Citigroup, AIG and Merrill Lynch). He's miffed because some institutions were "strong-armed" into merging with other institutions and taking government money. What Mr. Freey ignores is that the problem the financial sector created with their stupidity and greed is so big that the industry can't unwind many of the complex instruments that people like him helped create.

The toxic garbage has spread throughout the industry like an STD and require forced measures.

There's more. But Mr. Frey needs to keep a couple of things in mind. People are not only losing their jobs but they can do little to nothing as the value (and equity) of their homes collapse. Mr. Frey also needs to keep in mind that at least 1 million Americans will go bankrupt this year while many more see their credit wrecked for years to come. If Mr. Frey wants his "investment" guaranteed he should also be pushing to have the credit and value of each home owner's house guaranteed too. But he doesn't want this. All Mr. Frey is focused on is making sure that his money is guaranteed.

What a standup guy.

At the end of the day Mr. Freey needs to grow up, and learn one thing: there are no guarantees in life. He's not the only one affected by the mess people like him created.

- Mark

Tuesday, May 26, 2009

LET THE FEAR-MONGERING FEST BEGIN

It didn't take long, but it appears that Conservative commentators are already in full Liberal Fear-Mongering mode over President Obama's nomination for the Supreme Court, Sonia Sotomayor.

Do these guys even remember what it's like to have a discussion on the issues? Or are they so intellectually bankrupt that fear-mongering is all that they've got left? Seriously, they're afraid of al-Qaeda so they fear-monger over shredding the Constitution and the defense of torture ... they're afraid of homosexuals so they fear-monger over tolerance ... they're afraid of strong women and people of color so they fear-monger over "liberals" ... and on it goes.

At what point do Conservatives grow a pair and stop the fear-mongering? Just asking.

- Mark

Do these guys even remember what it's like to have a discussion on the issues? Or are they so intellectually bankrupt that fear-mongering is all that they've got left? Seriously, they're afraid of al-Qaeda so they fear-monger over shredding the Constitution and the defense of torture ... they're afraid of homosexuals so they fear-monger over tolerance ... they're afraid of strong women and people of color so they fear-monger over "liberals" ... and on it goes.

At what point do Conservatives grow a pair and stop the fear-mongering? Just asking.

- Mark

Saturday, May 23, 2009

OUR MEMORIAL DAY PROGRAM ... RETURNING VETERANS

Today we're going to have two segments. In the first hour we're scheduled to have Bakersfield Californian columnist Lois Henry with us. She'll be with us around 2:30 pm.

In the second hour we're going to celebrate our Memorial Day weekend with a discussion of how our injured and stress afflicted soldiers are doing when they come home from battle. We will interview United States Naval Reserve Commander (retired) Bill Manofsky. As a reservist Commander Manofsky volunteered to go on active duty to deploy to new targeting technologies for China Lake at the start of the war in Iraq, and was inserted into Special Forces Intelligence where he was subsequently injured in combat in 2003. Commander Manofsky was instrumental in helping to expose the problems of neglect at Walter Reed Hospital in Washington, D.C. Commander Manofsky is also a member of a the Iraq and Afghanistan veterans of America, the American Legion, and the VFW.

Also in the studio with us today will be Russ Sempell, who heads up FRONTLINE, which is a creation of Kern county's National Alliance of Mental Illness. FRONTLINE networks with individuals throughout the county and is committed to assisting Veterans and their families in the FAITH Community, in housing, obtaining benefits, educational training, accessing medical and behavioral health services, and other areas necessary for helping our returning soldiers make the transition from the battlefield.

You'll hear from Commander Manofsky and Mr. Sempell after the 3 o'clock hour.

- Mark

Thursday, May 21, 2009

CHENEY'S COWARDLY RESPONSE

Holy Paranoia Batman! Take a look at the fear-drenched nonsense that Dick Cheney just presented to the Republican Party’s “research” arm, the American Enterprise Institute (AEI). Here's the first problem: setting.

Dick Cheney can no longer go to applaud-guaranteed military bases to make scare-mongering speeches. So he has to go to places like AEI to make presentations that would, in all likelihood, be mocked and jeered in just about any other public setting. But we'll leave this one alone for the moment.

If you decide to take the time to read Dick Cheney’s extraordinarily long and self-serving speech what you will find is (1) a man who is focused on reliving 9/11 through eternity, and (2) a man who has no problem lying and leaving out key points that undermine the Bush administration’s claims, especially as they apply to national security. In a few words, Dick Cheney is a liar (see his WMD and al-Qaeda/Saddam-links comments) and a coward (five deferments when it was his turn to serve tells us this).

For me, this Cheney comment tells us what the former Vice-President has to say is baseless and drenched in self-serving hypocrisy …

Then we have this nonsense from Dick Cheney ...

The Bush administration had ample warning. They blew it. We were attacked on their watch in spite of their knowledge that "a series of terrorist plots" had occurred and top officials had told them that another one was coming. Saying we had to get tough because an attack occurred on their watch is akin to saying, "We need everyone to be afraid so they forget that we blew it."

There's more. Much more. But going through all Dick Cheney's nauseatingly long "let's-all-be-afraid-because-we-were-afraid" speech is a bloodletting experience we don't need to run through. The fact is, Dick Cheney has a history of cowardice and getting things wrong.

Cheney had his chance, and he helped make America weaker with his actions. He needs to let the adults clean up his mess.

- Mark

Dick Cheney can no longer go to applaud-guaranteed military bases to make scare-mongering speeches. So he has to go to places like AEI to make presentations that would, in all likelihood, be mocked and jeered in just about any other public setting. But we'll leave this one alone for the moment.

If you decide to take the time to read Dick Cheney’s extraordinarily long and self-serving speech what you will find is (1) a man who is focused on reliving 9/11 through eternity, and (2) a man who has no problem lying and leaving out key points that undermine the Bush administration’s claims, especially as they apply to national security. In a few words, Dick Cheney is a liar (see his WMD and al-Qaeda/Saddam-links comments) and a coward (five deferments when it was his turn to serve tells us this).

For me, this Cheney comment tells us what the former Vice-President has to say is baseless and drenched in self-serving hypocrisy …

"Releasing the interrogation memos was flatly contrary to the national security interest of the United States. The harm done only begins with top secret information now in the hands of the terrorists, who have just received a lengthy insert for their training manual. Across the world, governments that have helped us capture terrorists will fear that sensitive joint operations will be compromised. And at the CIA, operatives are left to wonder if they can depend on the White House or Congress to back them up when the going gets tough."Look, once the Bush administration – through Dick Cheney’s office – released the name of CIA asset Valerie Plame to teach her husband (Ambassador Joe Wilson) and others a lesson about what would happen if they crossed the administration Dick Cheney lost all moral standing when it comes to judging the actions of others in the area of national security. This is especially the case when the Obama administration is charged with trying to clean up the Bush administration’s mess caused by their unethical and illegal behavior.

Then we have this nonsense from Dick Cheney ...

"That attack itself was, of course, the most devastating strike in a series of terrorist plots carried out against Americans at home and abroad. In 1993, terrorists bombed the World Trade Center, hoping to bring down the towers with a blast from below. The attacks continued in 1995, with the bombing of U.S. facilities in Riyadh, Saudi Arabia; the killing of servicemen at Khobar Towers in 1996; the attack on our embassies in East Africa in 1998; the murder of American sailors on the USS Cole in 2000; and then the hijackings of 9/11, and all the grief and loss we suffered on that day."Where do I begin? The simplest response here is that the Bush administration didn’t do anything after they were briefed by outgoing National Security Advisor, Sandy Berger, and Counterterrorism Czar, Richard Clarke (who served Reagan, Bush I, and Clinton) made it clear that al Qaeda "would be your number one priority" during their tenure in office. They even ignored Richard Clarke, who was running around Washington DC during summer 2001 telling agency heads to cancel summer vacations because "something big" was going to happen. Then we have George W. Bush ignoring the CIA briefing titled "Bin Laden Determined to Attack U.S." ...

The Bush administration had ample warning. They blew it. We were attacked on their watch in spite of their knowledge that "a series of terrorist plots" had occurred and top officials had told them that another one was coming. Saying we had to get tough because an attack occurred on their watch is akin to saying, "We need everyone to be afraid so they forget that we blew it."

There's more. Much more. But going through all Dick Cheney's nauseatingly long "let's-all-be-afraid-because-we-were-afraid" speech is a bloodletting experience we don't need to run through. The fact is, Dick Cheney has a history of cowardice and getting things wrong.

Cheney had his chance, and he helped make America weaker with his actions. He needs to let the adults clean up his mess.

- Mark

OBAMA'S NATIONAL SECURITY SPEECH

In a blunt and forceful review of the previous administration's war on terror policies, President Obama outlined the vision and policy approach that his administration would follow. He did so against the backdrop of the National Archives Building in Washington, which houses the U.S. Constitution.

I watched the first part of it on television while the kids were eating breakfast and have to say it was a triumph of American values and moral inspiration. President Obama recognizes that America is more than a nation-state with weapons and a powerful military. We are also a nation of ideas that inspires in others what previous empires, civilizations, and dynasties could not.

What I particularly enjoyed was when he said that our policies should not be driven by fear ... In a few words, he gets it.

- Mark

Tuesday, May 19, 2009

MORE JESSE VENTURA ...

Sean Hannity's still a whiny coward.

He begins his interview with Jesse Ventura by trying to play nice with the former governor, softening him up with talk about surfing. Then Hannity says he doesn't want to go down the "old road" because he knows Ventura doesn't respect Bush or Cheney, so he asks "What do you think about Barack Obama?". He does this so he can talk about budget deficits and "teleprompters." Hannity then blames President Obama for what he inherited, and claims America is better off after the Bush years.

To his credit, Ventura kept Hannity on his heals by calling Hannity on his budget and teleprompter nonsense, among others. So what does Hannity do? He ends the interview by accusing Ventura of going down the "old road" because of how Ventura responded to Hannity's stupidity by pointing out that the Bush administration left President Obama an economic and military disaster - as if Ventura should have just let Hannity spout his ignorance without responding.

What a whiny coward.

- Mark

He begins his interview with Jesse Ventura by trying to play nice with the former governor, softening him up with talk about surfing. Then Hannity says he doesn't want to go down the "old road" because he knows Ventura doesn't respect Bush or Cheney, so he asks "What do you think about Barack Obama?". He does this so he can talk about budget deficits and "teleprompters." Hannity then blames President Obama for what he inherited, and claims America is better off after the Bush years.

To his credit, Ventura kept Hannity on his heals by calling Hannity on his budget and teleprompter nonsense, among others. So what does Hannity do? He ends the interview by accusing Ventura of going down the "old road" because of how Ventura responded to Hannity's stupidity by pointing out that the Bush administration left President Obama an economic and military disaster - as if Ventura should have just let Hannity spout his ignorance without responding.

What a whiny coward.

- Mark

CALIFORNIA ... THE UNGOVERNABLE STATE?

By way of Candi Easter, I was alerted to this Economist article on the problems facing California. It's one of the best reviews I've seen on the challenges facing California in years. Here's a snippet ...

California has a unique combination of features which, individually, are shared by other states but collectively cause dysfunction. These begin with the requirement that any budget pass both houses of the legislature with a two-thirds majority. Two other states, Rhode Island and Arkansas, have such a law. But California, where taxation and budgets are determined separately, also requires two-thirds majorities for any tax increase. Twelve other states demand this. Only California, however, has both requirements.Ultimately, as the article points out, California has dug itself into a political and budgetary hole. For some of you the article might be a bit long, but it's worth the read.

If its representative democracy functioned well, that might not be so debilitating. But it does not. Only a minority of Californians bother to vote, and those voters tend to be older, whiter and richer than the state’s younger, browner and poorer population, says Steven Hill at the New America Foundation, a think-tank that is analysing the options for reform.

Those voters, moreover, have over time “self-sorted” themselves into highly partisan districts: loony left in Berkeley or Santa Monica, for instance; rabid right in Orange County or parts of the Central Valley. Politicians have done the rest by gerrymandering bizarre boundaries around their supporters. The result is that elections are won during the Republican or Democratic primaries, rather than in run-offs between the two parties. This makes for a state legislature full of mad-eyed extremists in a state that otherwise has surprising numbers of reasonable citizens.

- Mark

Monday, May 18, 2009

DISBAR THE TORTURE LAWYERS

I like this ...

Twelve former Bush administration lawyers, who helped craft and justify the administration's torture policy, are named in a complaint that calls for them to be disbarred (which effectively prohibits them from practicing law).

According to Raw Story, the complaints were filed against former White House Legal Counsel attorneys John Yoo, Jay Bybee and Stephen Bradbury; former Attorney Generals Alberto Gonzales, John Ashcroft and Michael Mukasey; former Homeland Security Secretary Michael Chertoff; former chief of staff to Vice President Dick Cheney David Addington, Alice Fisher, William Haynes II, Douglas Feith and Timothy Flanigan with the state bars in the District of Columbia, New York, California, Texas and Pennsylvania.

The complaint says, in part, "We have asked the respective state bars to revoke the licenses of the foregoing attorneys for moral turpitude" because they "failed to show ‘respect for and obedience to the law, and respect for the rights of others,’ and intentionally or recklessly failed to act competently, all in violation of legal Rules of Professional Conduct.”

While legal incompetence is pretty strong, accusing these people of "moral turpitude" sounds about right too.

- Mark

Saturday, May 16, 2009

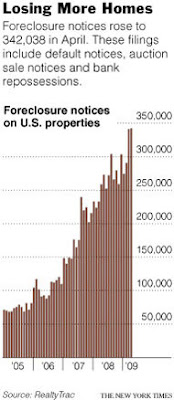

A SNAPSHOT OF FORECLOSURE & DEBT

The NY Times has two insightful articles dealing with the economic meltdown and the mortgage mess. "Slow Start to U.S. Plan for Modifying Mortgages" explains why foreclosures continue to rise by pointing to a system that is overwhelmed. It also makes it clear (at least to me) that the financial institutions really have no incentive to modify loans.

While the article doesn't do a good job spelling it out, part of the reason the financial instituitons aren't modifying loans or renegotiating in good faith is that they know they have access to U.S. taxpayer dollars, and don't have to worry about any real pressure from bankruptcy courts or the federal government, who continue to bail them out (which is another reason we should have nationalized the failing institutions). The end result is that home foreclosures continue to climb in spite of trillions in bailouts for the banks and billions that were made available to stave off foreclosure.

The second article worth reading is from the Times' economics reporter, Edmund L. Andrews. In "My Personal Credit Crisis" Andrews writes about his mortgage/debt nightmare.

In a surprisingly frank and personal review of how he got in over his head, Andrews provides an overview of how a combination of easy money, industry myopia, and wishful thinking on his part has driven him to the point of foreclosure, and bankruptcy. One thing is clear: blaming the debtor is not sufficient for understanding the mess he's (we're) in.

Read both articles. They also help us understand why the "stabilizing" economic picture painted by some analysts may be wildly optimistic, and even naive.

- Mark

While the article doesn't do a good job spelling it out, part of the reason the financial instituitons aren't modifying loans or renegotiating in good faith is that they know they have access to U.S. taxpayer dollars, and don't have to worry about any real pressure from bankruptcy courts or the federal government, who continue to bail them out (which is another reason we should have nationalized the failing institutions). The end result is that home foreclosures continue to climb in spite of trillions in bailouts for the banks and billions that were made available to stave off foreclosure.

The second article worth reading is from the Times' economics reporter, Edmund L. Andrews. In "My Personal Credit Crisis" Andrews writes about his mortgage/debt nightmare.

In a surprisingly frank and personal review of how he got in over his head, Andrews provides an overview of how a combination of easy money, industry myopia, and wishful thinking on his part has driven him to the point of foreclosure, and bankruptcy. One thing is clear: blaming the debtor is not sufficient for understanding the mess he's (we're) in.

Read both articles. They also help us understand why the "stabilizing" economic picture painted by some analysts may be wildly optimistic, and even naive.

- Mark

CREDIT CARD PSYCHOLOGY 101

The NY Times has an excellent article on credit card companies and how they have changed over the past 25 years. Here's a snippet.

Just a little more than two decades ago, the credit-card business was a quiet, slightly boring industry dominated by banks looking for easy revenue. Card issuers made money by collecting annual dues and interest payments from cardholders as well as fees from merchants each time a customer used a card. Then the math whizzes arrived. They emphasized that the biggest profits didn’t come from people who always paid off their bills but rather from less-responsible clients who never paid their entire balance, and thus could be milked through silently skyrocketing interest rates, late fees and other penalties. Since 1995, the percentage of the industry’s income from cardholder fees has more than doubled to 40 percent.The article is really a nice window into the psychology behind the industry, and how they use your purchasing history to determine credit limits and interest rate hikes. There's also some good information for those looking to negotiate with the credit card companies.

- Mark

Friday, May 15, 2009

STEWART MOCKS "DON'T ASK, DON'T TELL"

If we've bent the rules and compromised our moral standards with torture because of the war on terror John Stewart of the Daily Show asks why we can't allow gays in the military - especially those who speak Arabic. This line stands out.

While it's not on the clip, this one was pretty good too.

- Mark

... during this war on terrorism we've done nothing but make exceptions to the law ... warrantless wiretappings, suspending habeus corpus in situations, secret prisons, renditions to countries that torture ...In the video below Stewart mocks the U.S. military's absurd "don't ask, don't tell" policy which recently forced the firing of yet another gay officer (Daniel Choi) who speaks Arabic.

| The Daily Show With Jon Stewart | M - Th 11p / 10c | |||

| Dan Choi Is Gay | ||||

| ||||

While it's not on the clip, this one was pretty good too.

"So it was okay to waterboard a guy 80 times but God forbid the guy who could understand what that prick was saying has a boyfriend? Waterboarding may make a prisoner talk, but it ain't gonna make him talk English."

- Mark

Thursday, May 14, 2009

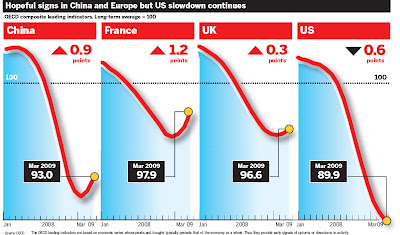

OUR CHALLENGE: CYCLICAL OR STRUCTURAL?

In yesterday's Bakersfield Californian I wrote that we shouldn't be doing any happy dances over claims that the U.S. economy seems to be recovering, or that the worst elements of a collapsing economy seem to be leveling out. In today's Financial Times' their sentiment for the global economy - which includes the U.S. - suggests there is a "pause" in the global economic slowdown.

As proof, the Times points to "long-term" economic indicators used by the Organisation for Economic Co-operation and Development (OECD) to project economic patterns (click on graph to expand).

Could I be off about the U.S. recession? Should we be preparing ourselves for a "pause" in the economic decline in the U.S.? Perhaps. But not for the reasons the OECD is suggesting. The insights of the OECD are determined by "growth cycle" trends, which may not be applicable given the type of meltdown we are currently experiencing. Specifically, what we are experiencing is tied to stupidity, greed, and a lack of regulation.

As far as I can see, the same market players who got us into this mess have not been fired, the same system of "reward" is in place, and the deregulation that took place in the 1980s and 1990s has not been rolled back. Then we have the massive consumer debt loads and stagnating wages confronting the American taxpayer.

Simply put, the problem is not cyclical, it's structural.

- Mark

UPDATE: Thanks to Mark Thoma's site, Economist's View, I've found a couple of articles that agree with me here and here.

As proof, the Times points to "long-term" economic indicators used by the Organisation for Economic Co-operation and Development (OECD) to project economic patterns (click on graph to expand).

Could I be off about the U.S. recession? Should we be preparing ourselves for a "pause" in the economic decline in the U.S.? Perhaps. But not for the reasons the OECD is suggesting. The insights of the OECD are determined by "growth cycle" trends, which may not be applicable given the type of meltdown we are currently experiencing. Specifically, what we are experiencing is tied to stupidity, greed, and a lack of regulation.

As far as I can see, the same market players who got us into this mess have not been fired, the same system of "reward" is in place, and the deregulation that took place in the 1980s and 1990s has not been rolled back. Then we have the massive consumer debt loads and stagnating wages confronting the American taxpayer.

Simply put, the problem is not cyclical, it's structural.

- Mark

UPDATE: Thanks to Mark Thoma's site, Economist's View, I've found a couple of articles that agree with me here and here.

NATIONAL SECURITY, OR CYA?

House Speaker Nancy Pelosi asserted today that the C.I.A. had "misled" Congress about its techniques. At the same time Pelosi acknowledged she learned that the CIA had subjected suspects to waterboarding in 2003.

Colin Powell's former Chief of Staff, Col. Lawrence Wilkerson, comments yesterday should help open Pandora's Box on the relationship between torture and the Bush administration's real goals behind torture (if the press can piece together the pieces):

- Mark

UPDATE: It appears that evidence for using torture to uncover a "Saddam-Al qaeda" link has Sea Legs ...

Colin Powell's former Chief of Staff, Col. Lawrence Wilkerson, comments yesterday should help open Pandora's Box on the relationship between torture and the Bush administration's real goals behind torture (if the press can piece together the pieces):

... what I have learned is that as the administration authorized harsh interrogation in April and May of 2002 -- well before the Justice Department had rendered any legal opinion -- its principal priority for intelligence was not aimed at pre-empting another terrorist attack on the U.S. but discovering a smoking gun linking Iraq and al-Qa'ida.In a few words, when it comes to torture, the Bush administration may not have been so concerned about national security as much as they were in CYA mode.

- Mark

UPDATE: It appears that evidence for using torture to uncover a "Saddam-Al qaeda" link has Sea Legs ...

*Two U.S. intelligence officers confirm that Vice President Cheney’s office suggested waterboarding an Iraqi prisoner, a former intelligence official for Saddam Hussein, who was suspected to have knowledge of a Saddam-al Qaeda connection.

*The former chief of the Iraq Survey Group, Charles Duelfer, in charge of interrogations, tells The Daily Beast that he considered the request reprehensible.

Tuesday, May 12, 2009

JESSE VENTURA: CHENEY'S A "COWARD"

Via Dailykos, former Minnesota Governor and Navy SEAL Jesse Ventura has some blunt commentary about the previous White House and torture ...

In case you can't watch the full interview (but I suggest you do), here's a couple of Ventura's comments.

In case you can't watch the full interview (but I suggest you do), here's a couple of Ventura's comments.

Ventura on Cheney avoiding service during the Vietnam War: "Clearly, he's a coward. He wouldn't go when it was his time to go."- Mark

Ventura on torture & waterboarding: "It's a good thing I'm not president ... I would prosecute every person involved in that torture. I would prosecute the people that did it. I would prosecute the people that ordered it. Because torture is against the law."

Ventura on former President George W. Bush: "the worst president of my lifetime. Barack Obama inherited something I wouldn't wish on my worst enemy."

THE $2 TRILLION MYSTERY

The Federal Reserve can't seem to account for how it has spent, or lent out, $2 trillion ...

I think it's an understatement to say this is not encouraging.

- Mark

I think it's an understatement to say this is not encouraging.

- Mark

Monday, May 11, 2009

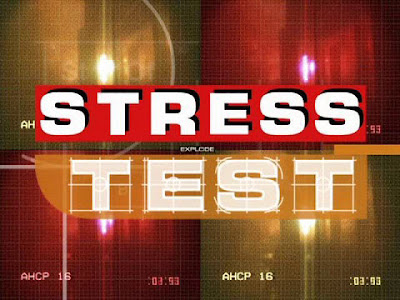

STRESS TESTS & NATIONALIZATION

Want to read some mind-numbingly laid-back specs for the banking industry? Take a look at the methodology outlined by the Federal Reserve for the infamous "stress tests" that banks are supposed to follow.

Ultimately, the goal is for troubled banks to provide information that will give us an idea as to whether they could survive several "stressful" economic scenarios. The pathetically low standards for the Stress Tests - also known as The Supervisory Capital Assessment Program: Design and Implementation - are only matched by the program's willful ignorance of the banking system's insolvency. Jule Satow outlines some of the problems here:

1. Banks Get to Determine Risk-Weighted Asset Values: Are you kidding me? We have to accept what the banks - who have been so good at honoring their fiduciary responsibilities in the past - say their toxic assets are worth? They're already loathe to renegotiate troubled home mortgage contracts because they don't want to reduce the value of their loan portfolios, so to expect the banks to be honest with us about their total assets because "it's the right thing to do" is asking for trouble.

2. Debt-to-Capital Ratio of 25 to 1 are Allowed: This is far higher than the 12 to 1 ratio that the SEC required of banks before the fateful 2004 decision that allowed the five largest investment banks to increase debt loads (discussed in Chapter 12 of my book, p. 275).

3. An 8.5% Loss Rate for Commercial Real Estate Portfolios: This not only depends on consumer spending picking up (have you seen consumer debt loads?) but is a very generous standard since default rates on commercial real estate have quintupled since the beginning of 2008.

Making matters worse is that little to nothing is said about the $50 trillion (about 3 x's our nation's GDP) in derivative trash that's still on the books ... or that several of the largest bank's exposure to derivatives exceed their total assets ... or that the FDIC is essentially running on fumes with approximately $50 billion left to cover 8,000 banks with about $7 trillion in deposits ... or that many of our financial institutions are pretty much insolvent zombie banks without the Fed's life support.

With these embarrassingly weak standards, and developing realities, I'm surprised that the Stress Tests don't require bankers to take a vacation in Tahiti. You know, to take the edge off of their stressful days from making stuff up.

Seriously, as Anthony Citrano suggests, the stress tests are akin to you going to your medical doctor for a physical that you need to pass for your job (after you've spent a year partying and eating as if you were in a Roman orgy) then having your doctor ask you if you want a clean bill of health.

Look, unlike Rush Limbaugh and the Republicans in Washington, I want President Obama to succeed. We need to nationalize failing institutions and the zombie banks, which will allow us to force failure on the clowns and the toxic instruments they helped create.

Unless the banks are weaned from government life support, these Stress Tests do little more than tell us what the banks want us know.

- Mark

Ultimately, the goal is for troubled banks to provide information that will give us an idea as to whether they could survive several "stressful" economic scenarios. The pathetically low standards for the Stress Tests - also known as The Supervisory Capital Assessment Program: Design and Implementation - are only matched by the program's willful ignorance of the banking system's insolvency. Jule Satow outlines some of the problems here:

1. Banks Get to Determine Risk-Weighted Asset Values: Are you kidding me? We have to accept what the banks - who have been so good at honoring their fiduciary responsibilities in the past - say their toxic assets are worth? They're already loathe to renegotiate troubled home mortgage contracts because they don't want to reduce the value of their loan portfolios, so to expect the banks to be honest with us about their total assets because "it's the right thing to do" is asking for trouble.

2. Debt-to-Capital Ratio of 25 to 1 are Allowed: This is far higher than the 12 to 1 ratio that the SEC required of banks before the fateful 2004 decision that allowed the five largest investment banks to increase debt loads (discussed in Chapter 12 of my book, p. 275).

3. An 8.5% Loss Rate for Commercial Real Estate Portfolios: This not only depends on consumer spending picking up (have you seen consumer debt loads?) but is a very generous standard since default rates on commercial real estate have quintupled since the beginning of 2008.

Making matters worse is that little to nothing is said about the $50 trillion (about 3 x's our nation's GDP) in derivative trash that's still on the books ... or that several of the largest bank's exposure to derivatives exceed their total assets ... or that the FDIC is essentially running on fumes with approximately $50 billion left to cover 8,000 banks with about $7 trillion in deposits ... or that many of our financial institutions are pretty much insolvent zombie banks without the Fed's life support.

With these embarrassingly weak standards, and developing realities, I'm surprised that the Stress Tests don't require bankers to take a vacation in Tahiti. You know, to take the edge off of their stressful days from making stuff up.

Seriously, as Anthony Citrano suggests, the stress tests are akin to you going to your medical doctor for a physical that you need to pass for your job (after you've spent a year partying and eating as if you were in a Roman orgy) then having your doctor ask you if you want a clean bill of health.

Look, unlike Rush Limbaugh and the Republicans in Washington, I want President Obama to succeed. We need to nationalize failing institutions and the zombie banks, which will allow us to force failure on the clowns and the toxic instruments they helped create.

Unless the banks are weaned from government life support, these Stress Tests do little more than tell us what the banks want us know.

- Mark

Sunday, May 10, 2009

WHITE HOUSE CORRESPONDENTS' DINNER

Here are the clipped highlights of President Obama poking fun at the Republicans, Michael Steele, Rush Limbaugh and Dick Cheney during the White House Correspondents' Dinner ...

Here's the entire 16 minutes of President Obama's presentation ...

Finally, go (click) here to see what the Republicans, FOX News, and Rush Limbaugh will be whining about this week.

- Mark

Here's the entire 16 minutes of President Obama's presentation ...

Finally, go (click) here to see what the Republicans, FOX News, and Rush Limbaugh will be whining about this week.

- Mark

Saturday, May 9, 2009

THIS IS WHY WE HAVE GOVERNMENT ...

Using humor, this YouTube clip points out the obvious: When it comes to creating a viable society, our government has gotten more than a few things right.

As former Supreme Court jurist Oliver Wendell Holmes put it, "Taxes are the price we pay for a civilized society."

- Mark

As former Supreme Court jurist Oliver Wendell Holmes put it, "Taxes are the price we pay for a civilized society."

- Mark

Friday, May 8, 2009

MORE TORTURED LOGIC

Lawrence O'Donnell sat in for MSNBC's Ed Schultz and took one of President Bush's Designer Torturers on a ride through the administration's "we-didn't-torture-but-it-was-legal" nonsense.

Specifically, O'Donnell responds to David Rivkin's assertion that he understands what torture is by asking Rivkin if he's ever been in the military or tortured. Rivkin (a former Justice Department official under Bush I) said "No" and fell back on the argument that we did worse to our own military personnel, so what we did during the Bush II administration can't be torture. Conveniently Rivkin leaves out - and leaves it to O'Donnell to point out - that we tortured our own military personnel to prepare them for torture. Rivkin apparently didn't recogize (or ignored) that he's admitting that we tortured.

I assure you, if you're having trouble following this Alice in Wonderland logic, you're not alone. Still, it's fun to watch ...

- Mark

Specifically, O'Donnell responds to David Rivkin's assertion that he understands what torture is by asking Rivkin if he's ever been in the military or tortured. Rivkin (a former Justice Department official under Bush I) said "No" and fell back on the argument that we did worse to our own military personnel, so what we did during the Bush II administration can't be torture. Conveniently Rivkin leaves out - and leaves it to O'Donnell to point out - that we tortured our own military personnel to prepare them for torture. Rivkin apparently didn't recogize (or ignored) that he's admitting that we tortured.

I assure you, if you're having trouble following this Alice in Wonderland logic, you're not alone. Still, it's fun to watch ...

- Mark

BANKERS ... STILL RUNNING THE SHOW

Here's an interesting article on home foreclosures. In a few words it explains how banks and the investors who hold the securities that come from home mortgages prefer to hold on to bad loans rather than renegotiate them. It's pretty interesting. Their rationale is that if they renegotiate a $400,000 loan to, say, $300,000 they and other market players will lose money.

They don't care that they are the beneficiaries of the greatest bailout in human history. They don't care that the Obama administration has provided generous gurantees and write-offs because they screwed things up so bad. They don't care that homeowners can continue to stay in their homes. They don't even seem to recognize that they brought much of the market's collapse on themselves by offering home buyers "novel" home loans when they had no income, no job, and no assets (the NINJA loans).

What the banks and other market players are concerned about is that if they reduce the amount of the loans they have on the books they will have to write down their total assets.

... Since mortgages are listed on the banks' balance sheets at the value of the original loan, if they complete a short sale they must record a loss on their balance sheets. That would explain why banks drag the process out as long as possible.The article explains that banks and other market players are doing this because of the dynamics behind the Collateralized Debt Obligation (CDO) market. This is probably true (read the article to understand the CDO market). However, in my view, banks and other market players are also not willing to renegotate because they are, incredibly enough, holding out for something better.

Banks and market players (who think they're investors) are holding out for a Green Light that will allow them to revalue all the toxic loans (and securities) along, say, a four year average. In a few words, they think that by keeping bad loans on the books at, say, $400,000 they might be able to have them averaged up to $450,000 (or more) because the value of the contract (security/loans) may have once hovered around $600,000 over the past four years.

If you're having trouble figuring out why it might work out this way, think about the value of your home. It might be worth $325,000 today, but it might have been worth $600,000 two years ago. Can you imagine being given the option of selling your home today at its four year average (let's say $450,000) rather than it's market price today? Sweet deal, huh? Why in the world would you reestablish the value of your home to $325,000 when you could hold out for $450,000? This is exactly what the bankers and security holders (which hold thousands of mortgages just like yours) see, and want.

All of this is made possible by a nice little provision that was inserted into the first 2008 bailout (TARP I). I'll discuss this on tomorrow's program.

- Mark

Wednesday, May 6, 2009

INFLATION IS OUR FRIEND?

OK, I should have been a bit clearer in my previous post where I discussed economist Paul Krugman's take on why the United State might be able to escape a bout of inflation. Here's what I should have included ...

In a few words, Krugman writes in The Return of Depression Economics that Japan's history during the 1990s is critical to understand because Japan experienced a banking collapse, which was brought on by a speculative real estate bubble that popped. Shades of America in 2008-2009, right? The collapse was followed by a massive transfer of government (i.e. taxpayer) funds that resembled our stimulus program, and an interest rate reduction that kept the cost of money effectively at zero.

So what happened in Japan? Economic stagnation. Banks could/would not lend, stimulus money (or deficit spending) did not work, and people would not spend/invest. As Krugman points out, this is what economists call a "liquidity trap."

A liquidity trap, if I can continue to oversimplify, is cheap money coupled with no spending.

This explains, in part, what kept inflation low in Japan and - according to economists today - is what's keeping inflation relatively low in the United States today (I'm not sure I agree because of international considerations, but that's another story). Krugman's solution for getting out of our current liquidity trap is rather simple and, for some, a scary proposition: Inflation.

The first thing someone might think about when they think of inflation is that it has the same effect as if you started burning your money: you have less and less of it. This may be true. But according to Krugman (and other economists) if inflation occurs during a liquidity trap, and people are afraid their money will be worth less in the future, they will eventually be compelled (scared?) into spending and investing. Why sit on $1,000 today if it's only going to be worth $800 next year?

The first thing someone might think about when they think of inflation is that it has the same effect as if you started burning your money: you have less and less of it. This may be true. But according to Krugman (and other economists) if inflation occurs during a liquidity trap, and people are afraid their money will be worth less in the future, they will eventually be compelled (scared?) into spending and investing. Why sit on $1,000 today if it's only going to be worth $800 next year?

So, in a few words, we are left with two options. First, in spite of record deficits we can keep inflation at bay if we're willing to suffer through a liquidity trap of cheap money with little spending. Or, we can court inflation which will help convince market players to spend and invest.

An interesting set of options indeed.

- Mark

In a few words, Krugman writes in The Return of Depression Economics that Japan's history during the 1990s is critical to understand because Japan experienced a banking collapse, which was brought on by a speculative real estate bubble that popped. Shades of America in 2008-2009, right? The collapse was followed by a massive transfer of government (i.e. taxpayer) funds that resembled our stimulus program, and an interest rate reduction that kept the cost of money effectively at zero.

So what happened in Japan? Economic stagnation. Banks could/would not lend, stimulus money (or deficit spending) did not work, and people would not spend/invest. As Krugman points out, this is what economists call a "liquidity trap."

A liquidity trap, if I can continue to oversimplify, is cheap money coupled with no spending.

This explains, in part, what kept inflation low in Japan and - according to economists today - is what's keeping inflation relatively low in the United States today (I'm not sure I agree because of international considerations, but that's another story). Krugman's solution for getting out of our current liquidity trap is rather simple and, for some, a scary proposition: Inflation.

The first thing someone might think about when they think of inflation is that it has the same effect as if you started burning your money: you have less and less of it. This may be true. But according to Krugman (and other economists) if inflation occurs during a liquidity trap, and people are afraid their money will be worth less in the future, they will eventually be compelled (scared?) into spending and investing. Why sit on $1,000 today if it's only going to be worth $800 next year?

The first thing someone might think about when they think of inflation is that it has the same effect as if you started burning your money: you have less and less of it. This may be true. But according to Krugman (and other economists) if inflation occurs during a liquidity trap, and people are afraid their money will be worth less in the future, they will eventually be compelled (scared?) into spending and investing. Why sit on $1,000 today if it's only going to be worth $800 next year?So, in a few words, we are left with two options. First, in spite of record deficits we can keep inflation at bay if we're willing to suffer through a liquidity trap of cheap money with little spending. Or, we can court inflation which will help convince market players to spend and invest.

An interesting set of options indeed.

- Mark

Tuesday, May 5, 2009

DUELING PERSPECTIVES ON INFLATION

This is from Professor Thoma's site, Economist's View ...

Are we headed for a bout of inflation like we saw in the 1970s? Political economist Allan H. Meltzer seems to think so, as he points out in this NY Times' piece"Inflation Nation."

There's a few more exchanges but, it would appear, Krugman wins this one. If you want to understand why Japan didn't experience inflation after pumping tons of money into the economy (and how it could work out this way for the U.S.) see Krugman's book, The Return of Depression Economics

There's a few more exchanges but, it would appear, Krugman wins this one. If you want to understand why Japan didn't experience inflation after pumping tons of money into the economy (and how it could work out this way for the U.S.) see Krugman's book, The Return of Depression Economics

- Mark

Are we headed for a bout of inflation like we saw in the 1970s? Political economist Allan H. Meltzer seems to think so, as he points out in this NY Times' piece"Inflation Nation."

If President Obama and the Fed continue down their current path, we could see a repeat of those dreadful inflationary years.As evidence that the United States is heading for an inflationary wall Professor Meltzer offers the following.

Besides, no country facing enormous budget deficits, rapid growth in the money supply and the prospect of a sustained currency devaluation as we are has ever experienced deflation. These factors are harbingers of inflation.Paul Krugman refers to this ...

There's a few more exchanges but, it would appear, Krugman wins this one. If you want to understand why Japan didn't experience inflation after pumping tons of money into the economy (and how it could work out this way for the U.S.) see Krugman's book, The Return of Depression Economics

There's a few more exchanges but, it would appear, Krugman wins this one. If you want to understand why Japan didn't experience inflation after pumping tons of money into the economy (and how it could work out this way for the U.S.) see Krugman's book, The Return of Depression Economics- Mark

SAVAGE NATION BANNED IN UK

I'm not sure what to make of this ...

Talk show host Michael Savage, who recently claimed that illegal aliens are carriers of the swine flu and that he was going to avoid contact with them, is one of 22 people who have been banned from entering Britain since October. The British government decided to keep Savage out of the country once they concluded that Savage (and the other 21 people named) were "agents of extremism and intolerance."

You know, here in the U.S. there's absolutely nothing in the Constitution that prohibits you from making a fool out of yourself, which Savage seems to do on a regular basis. However, what we have here is Britain simply stating that Savage goes beyond clown status and view him as a threat to public safety.

I think we'll talk about this on Saturday.

- Mark

Talk show host Michael Savage, who recently claimed that illegal aliens are carriers of the swine flu and that he was going to avoid contact with them, is one of 22 people who have been banned from entering Britain since October. The British government decided to keep Savage out of the country once they concluded that Savage (and the other 21 people named) were "agents of extremism and intolerance."

You know, here in the U.S. there's absolutely nothing in the Constitution that prohibits you from making a fool out of yourself, which Savage seems to do on a regular basis. However, what we have here is Britain simply stating that Savage goes beyond clown status and view him as a threat to public safety.

I think we'll talk about this on Saturday.

- Mark

Saturday, May 2, 2009

WHO PAYS ...

Today a caller wanted to complain about two things: 1) that I made fun of Rep. Michelle Bachmann (R-MN) because she doesn’t know history and (2) that poor people are ruining this country because they don’t pay taxes.

I don’t apologize for making fun of Rep. Michelle Bachmann. Click here to see why.

As for the tax argument, my caller complained that the poor are “dependent” and don’t pay their fair share. It’s the standard right-wing mantra … I work hard, so why should I have to support those who don’t work. To his credit, my caller left out the standard reference to illegal aliens (perhaps because earlier I had trashed Glenn Beck, Jay Severin, and Rush Limbaugh for their xenophobic Mexican hate-mongering over the swine flu).

As for who pays taxes ...

While it’s true the bottom 50% of the wage earners pay just 2.99% of all income taxes, it’s also true that their share of the national income (about $1 trillion divided between 67.8 million workers) amounts to only 12.5%. What an atrocity, my caller might still have claimed, if we had not run out of time.

However, it was clear that my caller didn’t want to discuss that every worker has to pay 6.2% in social security taxes and 1.45% for Medicare, meaning that they do have to pay taxes out of their paycheck. In fact, approximately ¾ of U.S. households pay more in social security taxes than they do in income taxes.

What people also forget is that after they earn $102,000 per year high income earners don’t have to pay into social security. This allows at least 10% of national income to go untaxed. This explains why the average middle-income household pays 9.6% of its income in social security taxes, while households in the top 1% of income pay less than 2%.

There’s more (especially on the philosophy behind progressive taxation), but any further discussion on taxes would bore the hell out of you.

At the end of the day, as Supreme Court Justice Oliver Wendell Holmes pointed out, “taxes are the price we pay for a civilized society." Just as importantly, given the great infrastructures and public institutions we have created in this country, taxes have enabled us to make the investments that have created opportunity for all in this country.

- Mark

I don’t apologize for making fun of Rep. Michelle Bachmann. Click here to see why.

As for the tax argument, my caller complained that the poor are “dependent” and don’t pay their fair share. It’s the standard right-wing mantra … I work hard, so why should I have to support those who don’t work. To his credit, my caller left out the standard reference to illegal aliens (perhaps because earlier I had trashed Glenn Beck, Jay Severin, and Rush Limbaugh for their xenophobic Mexican hate-mongering over the swine flu).

As for who pays taxes ...

While it’s true the bottom 50% of the wage earners pay just 2.99% of all income taxes, it’s also true that their share of the national income (about $1 trillion divided between 67.8 million workers) amounts to only 12.5%. What an atrocity, my caller might still have claimed, if we had not run out of time.

However, it was clear that my caller didn’t want to discuss that every worker has to pay 6.2% in social security taxes and 1.45% for Medicare, meaning that they do have to pay taxes out of their paycheck. In fact, approximately ¾ of U.S. households pay more in social security taxes than they do in income taxes.

What people also forget is that after they earn $102,000 per year high income earners don’t have to pay into social security. This allows at least 10% of national income to go untaxed. This explains why the average middle-income household pays 9.6% of its income in social security taxes, while households in the top 1% of income pay less than 2%.

There’s more (especially on the philosophy behind progressive taxation), but any further discussion on taxes would bore the hell out of you.

At the end of the day, as Supreme Court Justice Oliver Wendell Holmes pointed out, “taxes are the price we pay for a civilized society." Just as importantly, given the great infrastructures and public institutions we have created in this country, taxes have enabled us to make the investments that have created opportunity for all in this country.

- Mark

Friday, May 1, 2009

BANK LOBBYISTS STILL OWN D.C.

If we needed further evidence that we don't live in a free market environment consider the following. On a 51-45 vote the U.S. Senate rejected a measure that would have allowed bankruptcy judges to reduce the principal owed on a home mortgage. This celebratory picture seems to capture the mood of the banking industry after they heard the news ...

More seriously, the idea behind the measure is tied to the following three arguments.

More seriously, the idea behind the measure is tied to the following three arguments.